Traders and investors hoping for good news did not get it from Fed chief Jerome Powell. Mr. Powell, in his prepared remarks to congress, let it be known that inflation is not where the FOMC wants it. The latest data may warrant an increase in the pace of rate hikes and that peak interest rates could be higher than the market is pricing in. Before the comments, the CME FedWatch tool was pricing in a 30% chance for another 50 basis point hike and for the peak to be 5.5% or higher. That’s up 50 basis points over the last 2 to 3 months and will move even higher.

“The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated,” Powell said in prepared remarks for his appearance on Capitol Hill. “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

What Higher Rates Means For The Market

Higher rates mean 2 things for the market and neither is good. On the one hand, the cost of business will be much higher, and mortgage rates are the best evidence of that. Rates for all lending is pegged to the FOMC’s target rate, which is rising. The average rate for a 30-year mortgage is already tickling the 7.5% level again and will likely move higher.

The uptick in mortgage rates has demand for mortgages, a leading indicator of home sales and new home construction, down to near-30-year lows and falling. That has the outlook for home building, construction materials, and adjacent industries in decline, bringing up the 2nd tidbit investors should take away from this news.

The outlook for S&P 500 (NYSEARCA: SPY) earnings will continue to trend lower, and the downtrend may accelerate. As it is, the consensus target for all 4 quarters of 2023, as reported by Factset, is trending lower. The 1st half of the year will see earnings growth decline by 4.0%, and the back half isn’t much better. The back half is expected to return to growth, but these estimates are trending lower, and Q3 is precariously close to turning negative. The outlook for the year is for EPS growth near 2.1%, but this figure is also falling and very near 0.0%. Regarding the S&P 500, the forward outlook for earnings growth, more than anything else, gets it moving. In this scenario, the outlook will lead the market lower, and the subsequent decline has already begun.

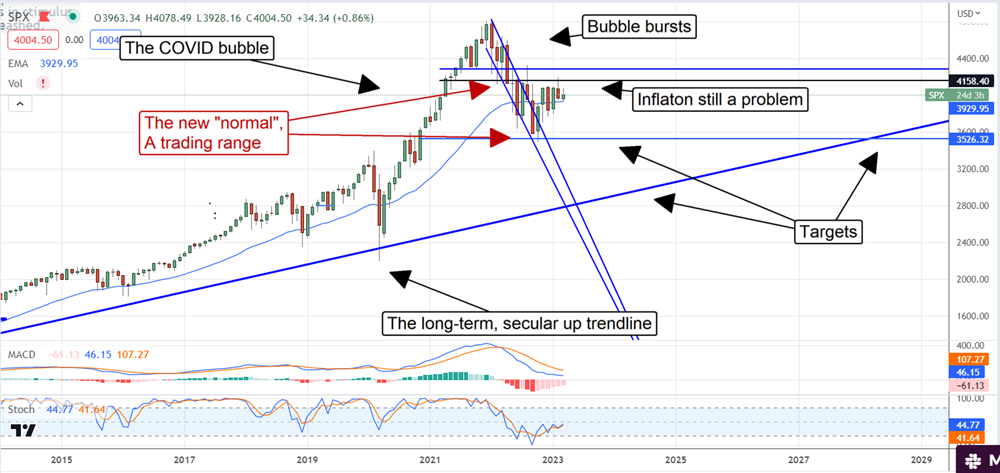

The Technical Outlook: The S&P 500 Is In A Rolling Bear Market

The market rally from October 2022 to February 2023 is nothing more than a bear-market rally. It was driven by the deceleration of inflation and the slowdown in interest rate hikes that it caused. In neither case was that good news, only less bad news, and now the news is worsening again. Investors should expect to see the S&P 500 trend lower soon, with a target near the bottom of the 2022/2023 trading range. That will put the S&P 500 down near 3,600, the next critical juncture. At that time, if the outlook for the back half of the year stabilizes or improves, the market could bottom and even rally within the range. If not, this market could fall through support to retest lower levels.

It is unlikely the S&P 500 will hit a new all-time high in the next year or 2. At best, investors should expect the market rotation to continue as industries consolidate and leadership positions are cemented. Periodic rallies and sell-offs may punctuate this rotation as the market returns to trend. The COVID-stimulus bubble was historical, and the following inflation is also historical; it will take a historic effort to put this genie back into the bottle.