If you're like most investors, retirement is one of your major financial goals. However, the road toward retirement can often seem overwhelming and confusing — especially regarding the many types of retirement accounts you can use to invest. An individual retirement account (IRA) is a tax-advantaged account you can use in conjunction with other retirement accounts to save more money toward your golden years.

What is an IRA, and how does it work? What can I do with an IRA account, and how does an IRA account vary from other major retirement investing accounts? If you're an investor asking these questions, you're not alone. Read on to learn more about IRA retirement investment options and what to do with IRA money when investing independently.

What is an IRA?

An IRA is a type of investment account that designed to help individuals save for retirement. IRAs were introduced as an additional retirement savings vehicle in 1974 as part of the Employee Retirement Income Security Act (ERISA). The same legislation created 401(k) plans, and both accounts have similar benefits. You can open an IRA through a major brokerage account provider like Vanguard, T.D. Ameritrade and Charles Schwab.

Like a 401(k), any IRA investment you make will have benefits when you file taxes or when you withdraw funds in retirement. There are multiple types of IRA accounts, with variations between accounts mainly coming down to contribution limits and when you are taxed on the investments you contribute to the account.

Why Invest in an IRA?

Now that you understand "what is an IRA account?", you might wonder why you need one. Multiple benefits come with investing through your IRA, including the following:

- Tax advantages: Depending on your IRA type, you can make tax-deductible contributions, reducing your total taxable income for the year. If you must pay taxes on your contributions, you can tax distributions tax-free.

- Investment flexibility: With an IRA, you can choose from a wider range of investment options, including individual stocks and bonds, mutual funds and ETFs. If your primary retirement account is an employer-sponsored 401(k), an IRA can provide greater flexibility.

- Can provide higher contribution limits: Investors can invest using an IRA and a 401(k). If you've maxed out your 401(k), an IRA can help you take advantage of more tax benefits.

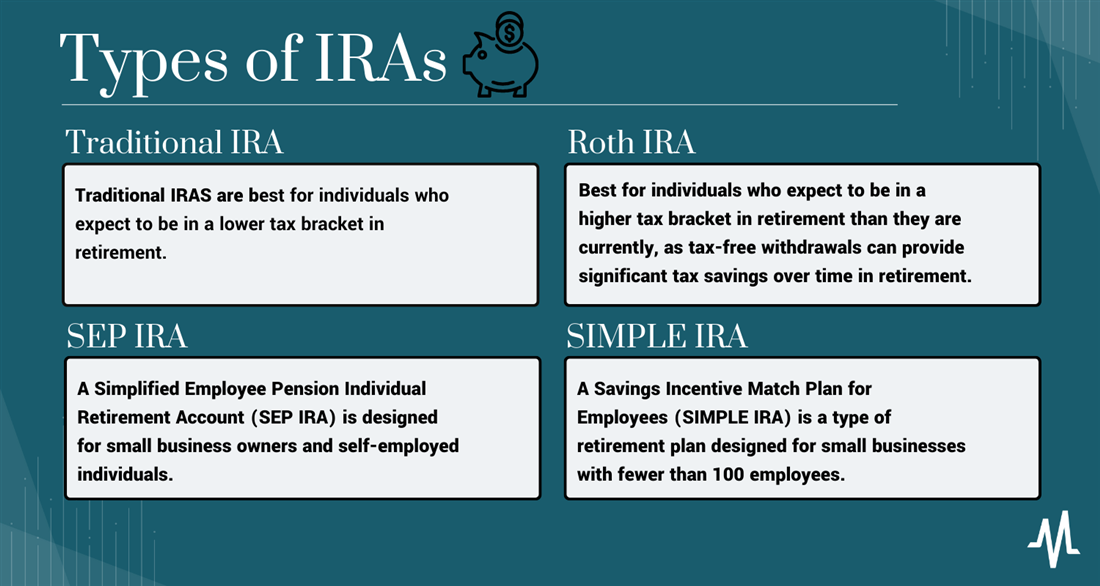

Types of IRAs

There are multiple types of IRAs, and the type of account that you open will determine when you can take tax benefits from your contributions and how your plan is managed. The following are the most common IRA options you'll see as you shop.

Traditional IRA

A traditional IRA is one of the most common types of IRA. With a traditional IRA, you can deduct your contributions from your annual taxable income. This can reduce your tax bill and provide an immediate tax benefit for contributing to the account by reducing the amount of money you must pay taxes on when you file.

Traditional IRAs are best for individuals who expect to be in a lower tax bracket in retirement than they are currently. The tax deduction for contributions provides an immediate benefit for reducing taxable income, and the taxes on withdrawals in retirement may be lower if you are in a lower tax bracket.

Roth IRA

A Roth IRA is a type of individual retirement account offering tax-free growth and retirement withdrawals. Contributions to a Roth IRA are made with after-tax dollars, so there is no immediate tax deduction. However, the money in the account grows tax-free, and withdrawals in retirement are also tax-free. Roth IRAs are best for individuals who expect to be in a higher tax bracket in retirement than they are currently, as tax-free withdrawals can provide significant tax savings over time in retirement.

SEP IRA

A Simplified Employee Pension Individual Retirement Account (SEP IRA) is designed for small business owners and self-employed individuals. With an SEP IRA, the employer makes contributions to the account on behalf of eligible employees, which are tax-deductible for the employer. SEP IRAs differ from other types because they have higher contribution limits, allowing employers to make larger contributions to the account.

SIMPLE IRA

A Savings Incentive Match Plan for Employees (SIMPLE IRA) is a type of retirement plan designed for small businesses with fewer than 100 employees. With a SIMPLE IRA, both the employer and the employee can make contributions to the account, and these contributions are tax-deductible for the employer and tax-deferred for the employee. The contribution limits for SIMPLE IRAs are lower than for other retirement accounts, but they are still higher than for traditional or Roth IRAs.

|

Account type |

Best for |

Annual contribution limit |

Tax benefits |

Required distributions |

|

Traditional IRA |

Anyone whose income will likely be lower in retirement |

$6,500 up to age 50 |

Deduct up to 100% of contributions during annual tax year |

Beginning at age 72 |

|

Roth IRA |

Anyone whose income will likely be higher in retirement |

$6,500 up to age 50 |

Contribute with post-tax income; non-taxable in retirement |

None |

|

SEP IRA |

Self-employed persons and freelancers |

Up to 25% of your income up to $61,000 |

Investment income is tax-deferred |

Beginning at age 72 |

|

SIMPLE IRA |

Small employers and business owners |

$15,500 up to age 50 |

Money grows tax-deferred until distributions |

Beginning at age 72 |

How Does an IRA Work?

Like any retirement plan with tax advantages, there are rules that you need to follow when contributing and taking distributions from an IRA. You'll need to follow the following major regulations when setting up and managing your IRA to avoid fees and penalties.

Deduction Limits

IRA deduction limits refer to the maximum amount of money you can contribute to an IRA each year and still be eligible for a tax deduction. The deduction limits for traditional IRAs are based on your income and tax filing status.

If you are single for the 2023 tax year, you can take a full contribution deduction if your modified adjusted gross income (MAGI) is $73,000 or less. The deduction amount decreases as your income increases, and you are not eligible for a deduction if your income is above $83,000.

Contribution Limits

Contribution limits refer to the maximum amount of money you can contribute to an IRA in a given year. The IRS sets the contribution limits for IRAs, which can change yearly depending on factors like inflation. The IRA contribution limit for 2023 is $6,500 for those under 50. If you're 50 or older, you may contribute up to $7,500 to your IRA in 2023.

Rollovers

If you want to consolidate multiple retirement accounts, consider a rollover. During an IRA rollover, you move money and assets from one retirement account to another. An IRA rollover must be supervised due to the tax-advantaged status of these accounts.

What is the IRA rollover process? To initiate an IRA rollover, contact the financial institution that holds your current retirement account and request a direct rollover to the new IRA account. The financial institution will then send the funds directly to the new IRA account, which can help to avoid taxes and penalties. This Roth IRA calculator from MarketBeat can help you choose where to open your account to save as much as possible.

Distributions

What is an IRA distribution? When you take an IRA distribution, you dissolve a portion of the assets in your account and take cash out to use for living expenses. You can take distributions at any time, but they are subject to certain rules and regulations depending on your IRA type.

For example, if you have a traditional IRA, distributions are subject to federal income tax, and you may also be subject to a 10% penalty if you withdraw funds before age 59 1/2. For Roth IRAs, distributions are tax-free if you have held the account for at least five years and are at least 59 1/2 when you take the distribution. Consult with a retirement professional if you're approaching retirement age and need advice on when to take distributions.

Pros and Cons of IRAs

Now that you understand the "what's an IRA," nuances, how it works and the type of financial contributions you can make in a year, it's time to think about how you can invest to meet your goals. As an investor, you have a limited amount of capital you can invest in each account. Consider both the pros and cons of investing through an IRA before opening an account.

Pros

- Tax benefits: No matter what type of IRA you open, you'll enjoy tax savings compared to other account types. For example, with a traditional IRA, your contributions can reduce your annual taxable income.

- More control over investment choices: If you open a self-directed IRA, you can choose your individual investments to include in the account.

- Flexibility: Most investors will still qualify for an IRA even if they have multiple other retirement accounts. For example, you might invest primary retirement savings into a 401(k), shop media sentiment stock lists through a taxable account and add extra tax-advantaged investments to an IRA.

Cons

- Withdrawal restrictions: IRAs have restrictions on when and how you can withdraw money without penalties, which can limit your access to your funds.

- Limited investment options: Depending on the financial institution that holds your IRA, your investment options may be limited to certain assets or mutual funds. If you're primarily interested in buying and selling stocks trending in the media, an IRA might not be your best investment option.

- Contribution limits: IRAs have contribution limits as low as $6,500 annually, limiting the amount of money you can save for retirement each year.

How to Get an IRA

Opening an IRA is relatively easy compared to other retirement accounts. To open an IRA, use the following basic steps.

Consider Account Type

First, decide which type of IRA is best for you based on your financial goals and tax situation. Most IRA providers offer multiple accounts, so choose your account type first.

Select a Broker

Once you've decided on the type of IRA you want to open, choose a financial institution that offers the type of IRA you want. In most cases, this will be a broker that offers other financial services. Fill out the application provided by the financial institution—most brokers now approve IRA applications filed online instantly.

Fund Your Account

After you establish your account, browse your broker's available IRA investment. Depending on where you've opened an account, you may be unable to buy and sell individual shares of stocks. Review fund and account fees before placing a purchase order, and monitor how your investment changes over time.

Investing with an IRA

Due to its lower limits on most accounts, IRAs are best used in conjunction with another type of retirement account. If you have a 401(k) that you max out annually, you can continue investing through an IRA. This can provide a more diverse range of tax protections.

FAQs

What are some frequently asked questions about IRAs? Let's take a look.

What is an IRA account, and how does it work?

An IRA is a tax-advantaged type of retirement account. IRA contributions may be invested in various assets, such as stocks, bonds and mutual funds, and the earnings grow tax-free or tax-deferred until retirement age. Once the account holder reaches retirement age, they can withdraw the funds, paying taxes on the distributions according to their type of IRA.

Is it better to have a 401(k) or IRA?

A 401(k) can be a good option for those who have access to one through their employer and want to contribute more than the annual IRA limit. An IRA can be a better option for those who want more control over their investments or don't have access to a 401(k). If you can have and fund both accounts, it's usually better.

What is the benefit of an IRA?

IRAs have tax advantages. Depending on your account type, you can deduct your contributions from your annual taxes or take the money tax-free.