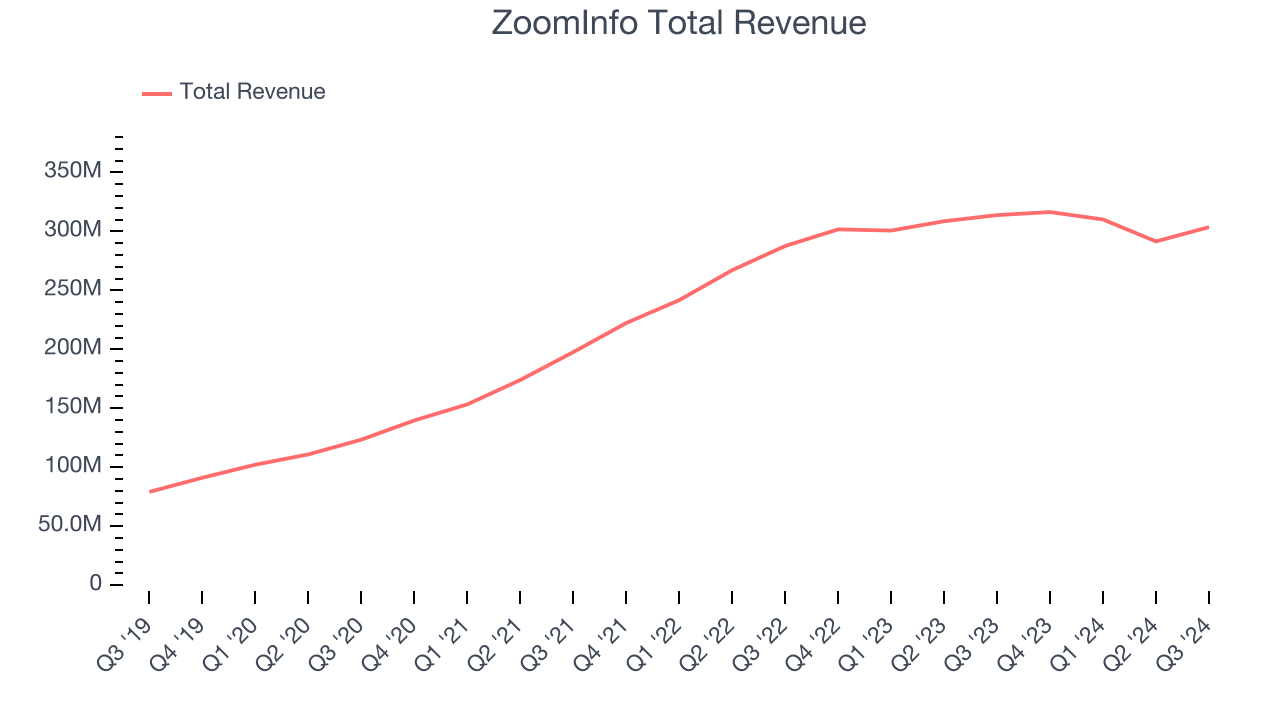

Sales intelligence platform ZoomInfo reported Q3 CY2024 results beating Wall Street’s revenue expectations, but sales fell 3.3% year on year to $303.6 million. The company expects next quarter’s revenue to be around $297.5 million, close to analysts’ estimates. Its non-GAAP profit of $0.28 per share was also 26.9% above analysts’ consensus estimates.

Is now the time to buy ZoomInfo? Find out by accessing our full research report, it’s free.

ZoomInfo (ZI) Q3 CY2024 Highlights:

- Revenue: $303.6 million vs analyst estimates of $299.3 million (1.4% beat)

- Adjusted EPS: $0.28 vs analyst estimates of $0.22 (26.9% beat)

- Adjusted Operating Income: $111.7 million vs analyst estimates of $107.7 million (3.7% beat)

- Revenue Guidance for Q4 CY2024 is $297.5 million at the midpoint, roughly in line with what analysts were expecting

- Management raised its full-year Adjusted EPS guidance to $0.93 at the midpoint, a 6.3% increase

- Gross Margin (GAAP): 87.6%, down from 88.8% in the same quarter last year

- Operating Margin: 14.3%, down from 20.1% in the same quarter last year

- Free Cash Flow Margin: 0.2%, down from 41.2% in the previous quarter

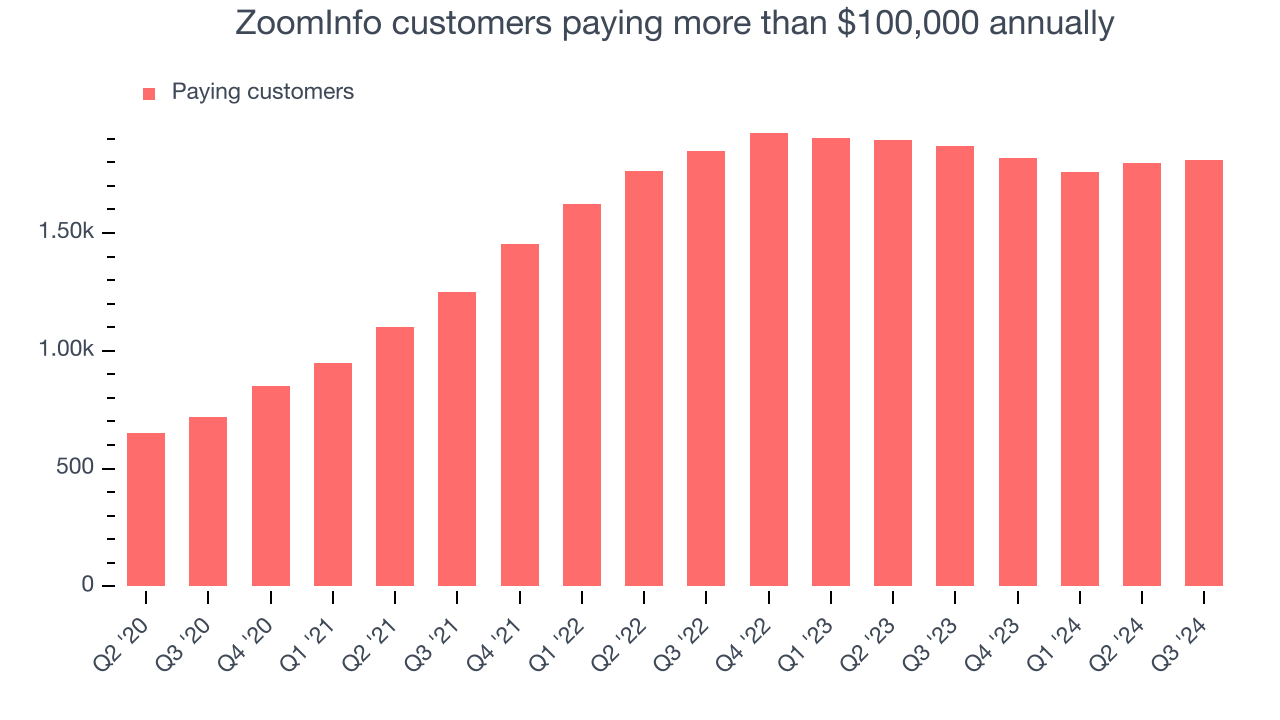

- Customers: 1,809 customers paying more than $100,000 annually

- Market Capitalization: $4.62 billion

“We continued our move up-market, fueled by ZoomInfo Copilot and Operations growth, and we delivered strong financial results while improving the quality of new customers that we are bringing in. The entire company is more focused than ever on delighting both our new and existing users via robust product innovation and customer obsession,” said Henry Schuck, ZoomInfo founder and CEO.

Company Overview

Founded in 2007 as DiscoveryOrg and renamed after a merger in 2019, ZoomInfo (NASDAQ:ZI) is a software as a service product that provides sales departments with access to a database of prospective clients.

Sales Software

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last three years, ZoomInfo grew its sales at a decent 22.5% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

This quarter, ZoomInfo’s revenue fell 3.3% year on year to $303.6 million but beat Wall Street’s estimates by 1.4%. Company management is currently guiding for a 6% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to decline 2.4% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Large Customers Growth

This quarter, ZoomInfo reported 1,809 enterprise customers paying more than $100,000 annually, an increase of 12 from the previous quarter. That’s a bit fewer contract wins than last quarter and quite a bit below what we’ve typically observed over the past four quarters, suggesting that its sales momentum with large customers is slowing.

Key Takeaways from ZoomInfo’s Q3 Results

We were impressed by ZoomInfo’s optimistic full-year EPS forecast, which exceeded analysts’ expectations. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter fell short of Wall Street’s estimates. The outlook is weighing on shares. Big picture, the market is worried that AI will be a huge headwind to ZoomInfo's business, and to convince the market otherwise, more convincing beats and guides above expectations are needed. The stock traded down 8.3% to $12 immediately following the results.

Is ZoomInfo an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.