Micron’s stock price has taken a beating over the past six months, shedding 23% of its value and falling to $98.35. Least to say, most shareholders are not pleased. This might have investors contemplating their next move.

Is now the time to buy Micron, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.Even though the stock has become cheaper, we're cautious about Micron. Here are three reasons why there are better opportunities than MU and one stock we like more.

Why Do We Think Micron Will Underperform?

Founded in the basement of a Boise, Idaho dental office in 1978, Micron (NYSE:MU) is a leading provider of memory chips used in thousands of devices across mobile, data centers, industrial, consumer, and automotive markets.

1. Long-Term Revenue Growth Disappoints

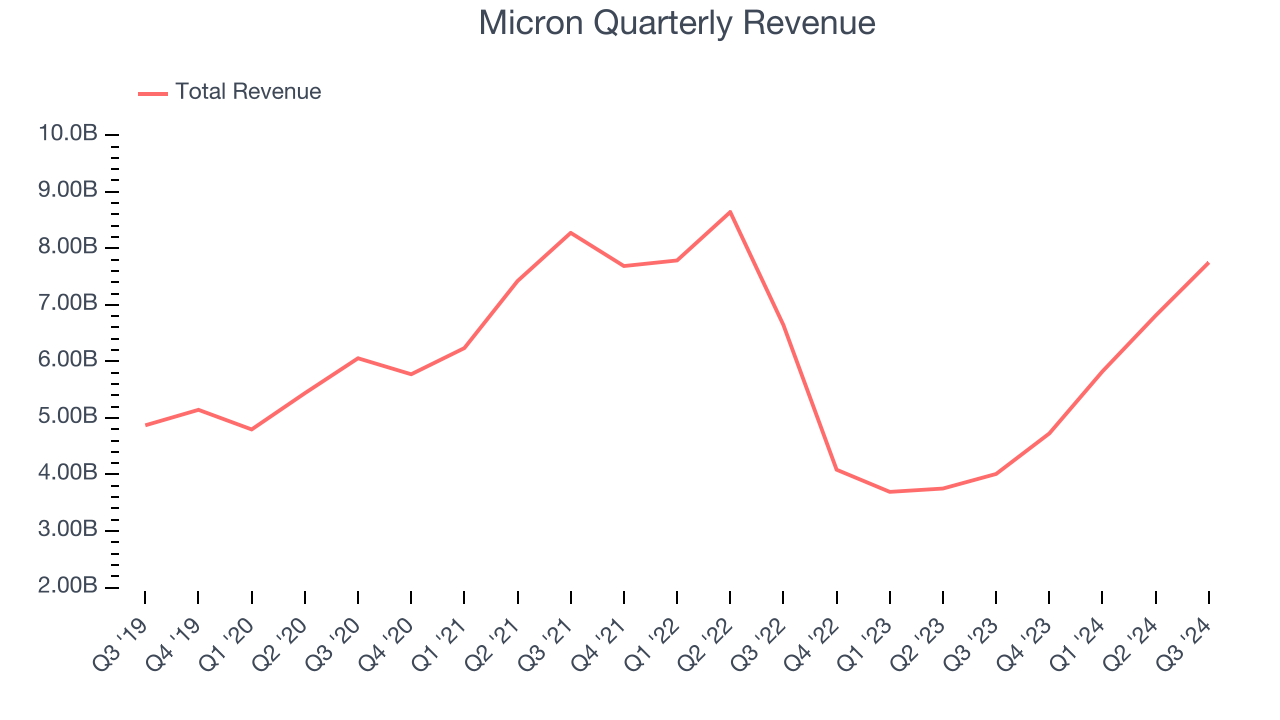

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Micron grew its sales at a weak 1.4% compounded annual growth rate. This shows it couldn’t expand in any major way. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

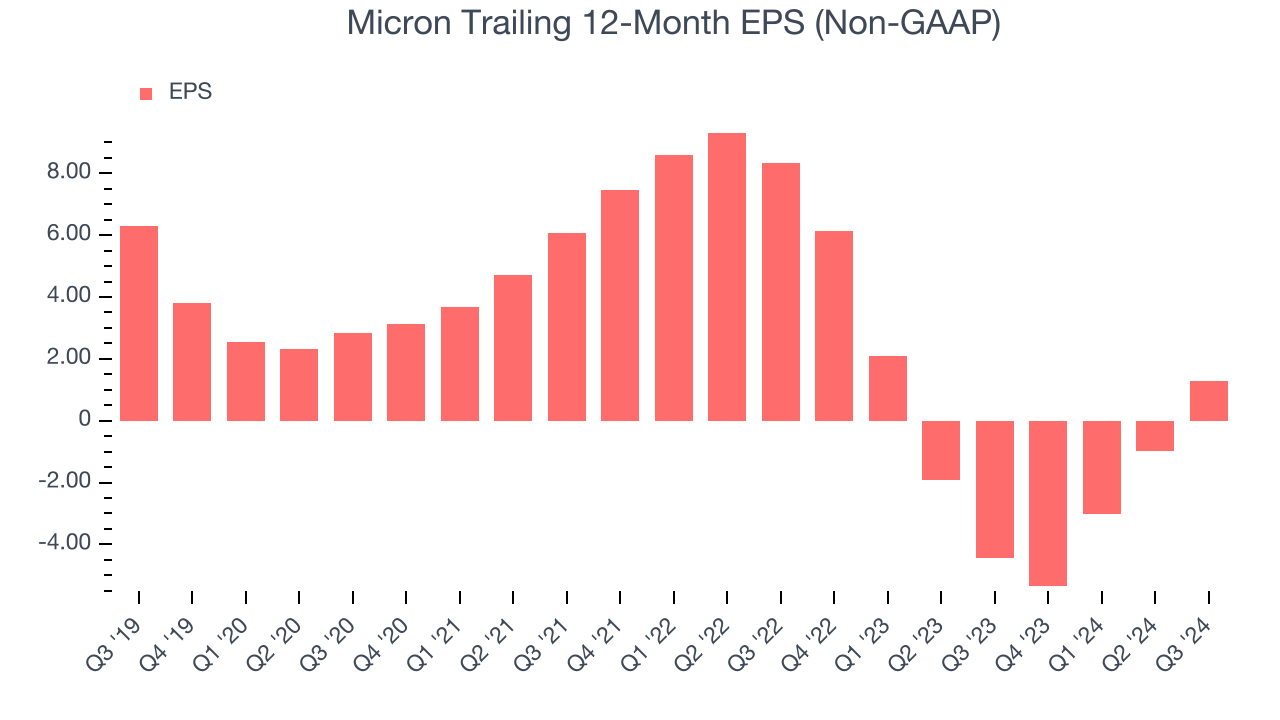

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth was profitable.

Sadly for Micron, its EPS declined by 27.4% annually over the last five years while its revenue grew by 1.4%. This tells us the company became less profitable on a per-share basis as it expanded.

3. Cash Burn Ignites Concerns

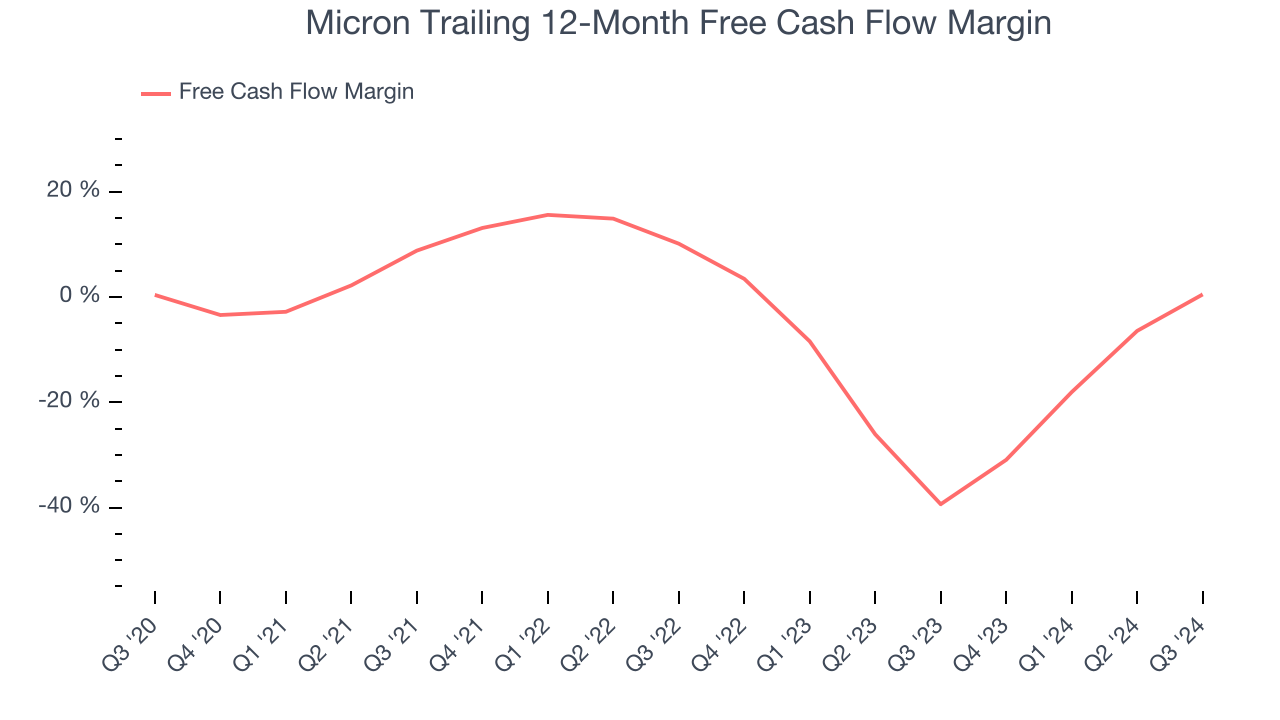

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Micron posted positive free cash flow this quarter, the broader story hasn’t been so clean. Micron’s demanding reinvestments have drained its resources over the last two years, putting it in a pinch and limiting its ability to return capital to investors.. Its free cash flow margin averaged negative 14.7%, meaning it lit $14.75 of cash on fire for every $100 in revenue.

Final Judgment

We see the value of companies furthering technological innovation, but in the case of Micron, we’re out. Following the recent decline, the stock trades at 11.6x forward price-to-earnings (or $98.35 per share). This multiple tells us a lot of good news is priced in - you can find better investment opportunities elsewhere. Let us point you toward Costco, one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Micron

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our High Quality Stocks with strong momentum. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.