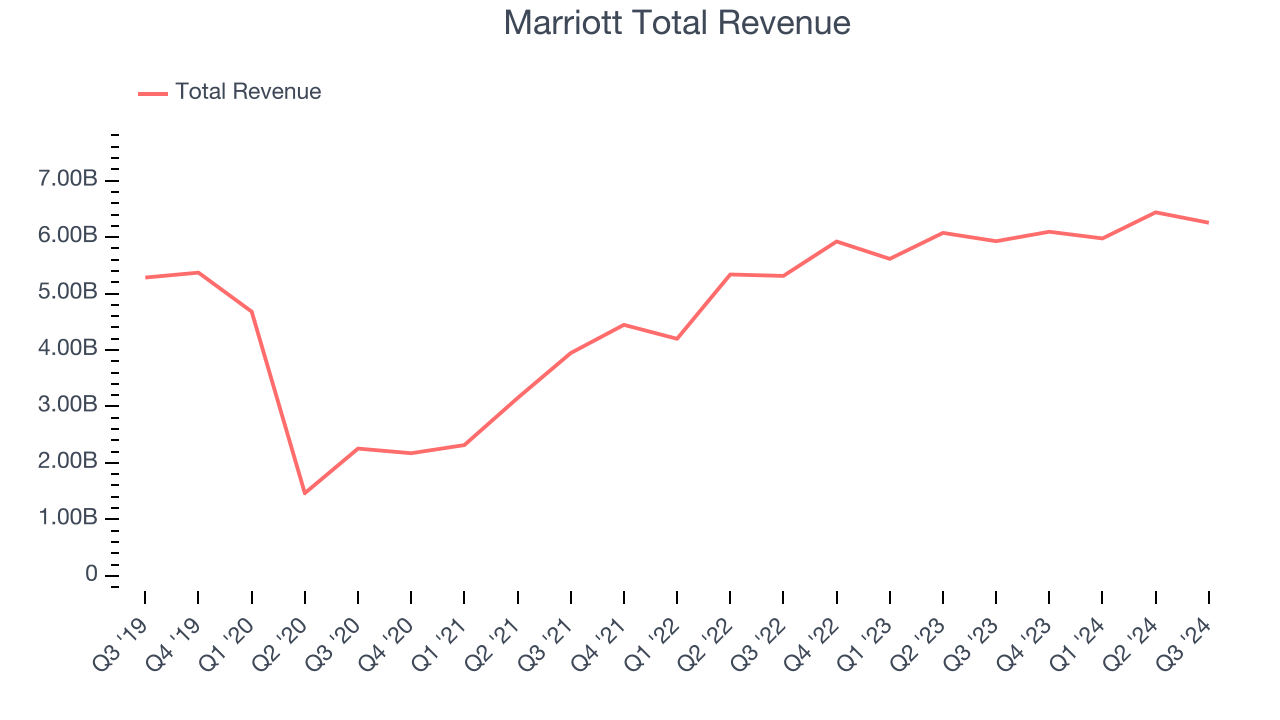

Global hospitality company Marriott (NASDAQ:MAR) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 5.5% year on year to $6.26 billion. Its non-GAAP profit of $2.26 per share was 2.1% below analysts’ consensus estimates.

Is now the time to buy Marriott? Find out by accessing our full research report, it’s free.

Marriott (MAR) Q3 CY2024 Highlights:

- Revenue: $6.26 billion vs analyst estimates of $6.26 billion (in line)

- Adjusted EPS: $2.26 vs analyst expectations of $2.31 (2.1% miss)

- EBITDA: $1.23 billion vs analyst estimates of $1.24 billion (small miss)

- Management lowered its full-year Adjusted EPS guidance to $9.23 at the midpoint, a 0.9% decrease

- EBITDA guidance for the full year is $4.95 billion at the midpoint, below analyst estimates of $4.99 billion

- Gross Margin (GAAP): 95.2%, in line with the same quarter last year

- Operating Margin: 15.1%, down from 18.5% in the same quarter last year

- EBITDA Margin: 19.6%, in line with the same quarter last year

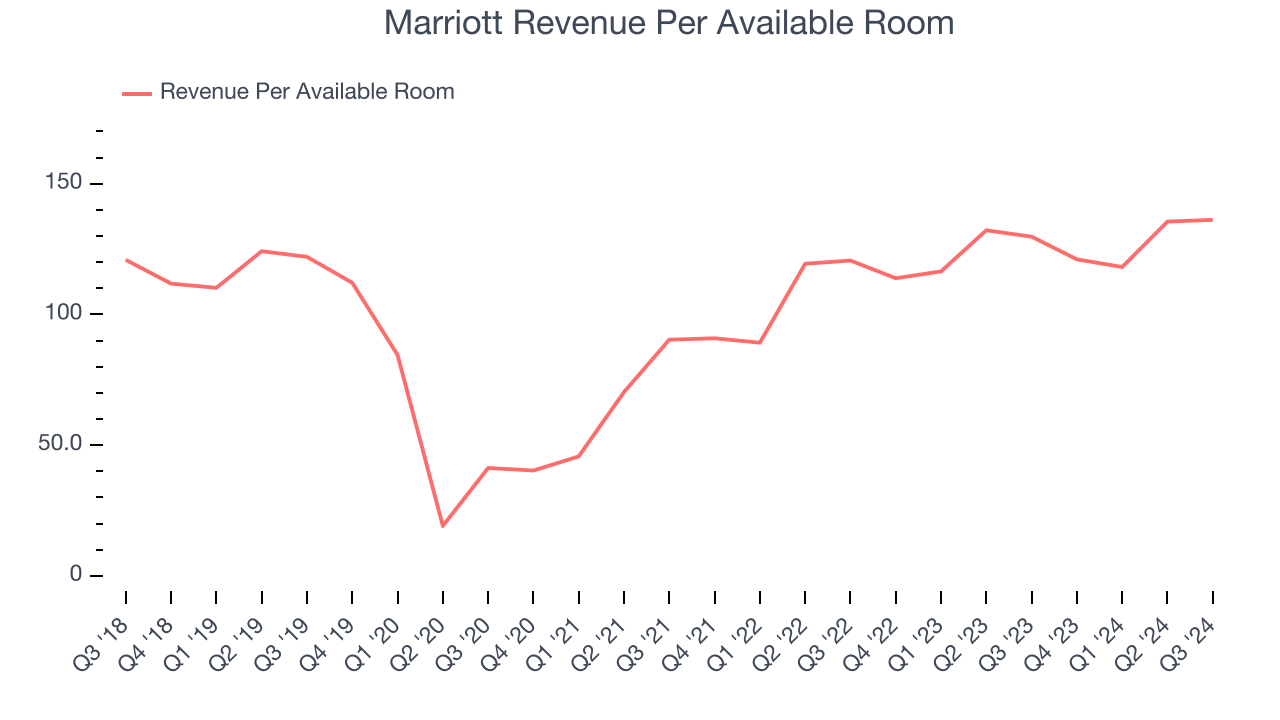

- RevPAR: $136.15 at quarter end, up 4.9% year on year

- Market Capitalization: $73.36 billion

Anthony Capuano, President and Chief Executive Officer, said, "Marriott had another solid quarter, highlighted by strong net rooms and fee growth, robust development activity and a 3 percent increase in global RevPAR1. Third quarter international RevPAR rose 5.4 percent, led by meaningful gains in APEC and EMEA with resilient domestic and cross-border demand, as well as solid ADR growth. RevPAR in the U.S. & Canada increased more than 2 percent compared to the year-ago quarter, with ADR up 2.3 percent.

Company Overview

Founded by J. Willard Marriott in 1927, Marriott International (NASDAQ:MAR) is a global hospitality company with a portfolio of over 7,000 properties and 30 brands, spanning 130+ countries and territories.

Travel and Vacation Providers

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

Sales Growth

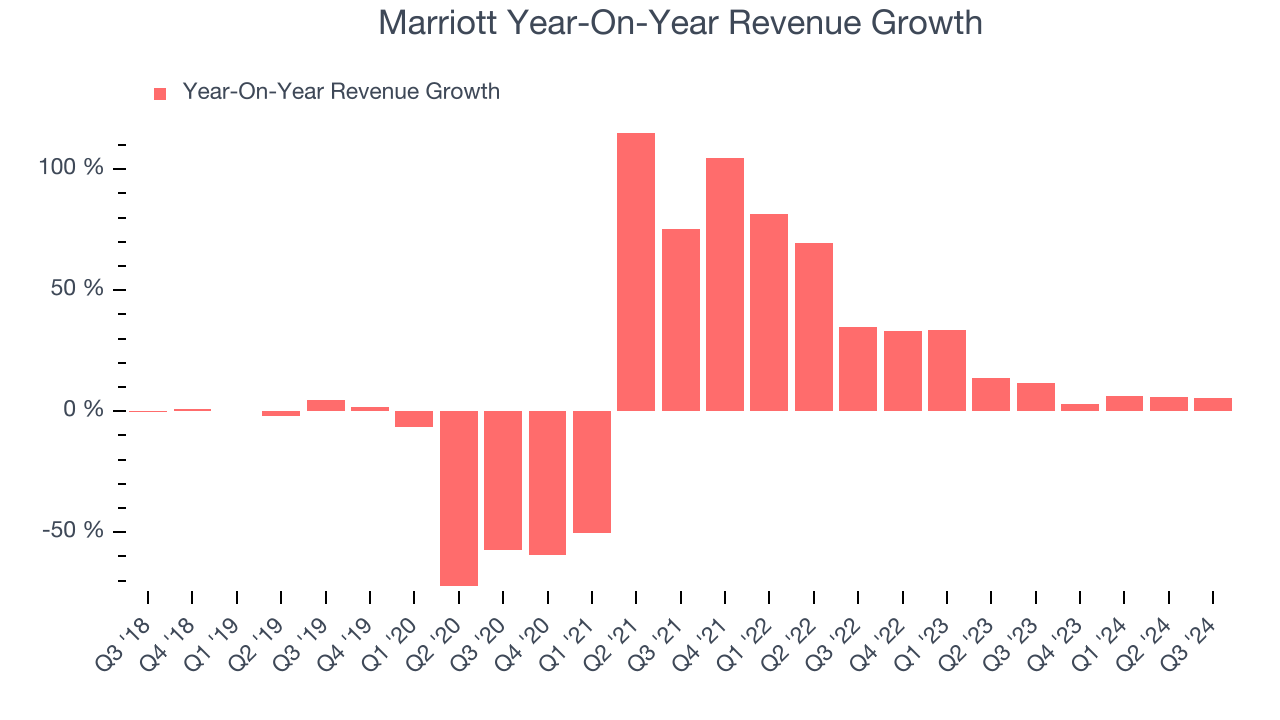

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Marriott’s 3.5% annualized revenue growth over the last five years was sluggish. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or emerging trend. Marriott’s annualized revenue growth of 13.3% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can better understand the company’s revenue dynamics by analyzing its revenue per available room, which clocked in at $136.15 this quarter and is a key metric accounting for daily rates and occupancy levels. Over the last two years, Marriott’s revenue per room averaged 11.2% year-on-year growth. Because this number is lower than its revenue growth, we can see its sales from other areas like restaurants, bars, and amenities outperformed its room bookings.

This quarter, Marriott grew its revenue by 5.5% year on year, and its $6.26 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and illustrates the market believes its products and services will see some demand headwinds.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

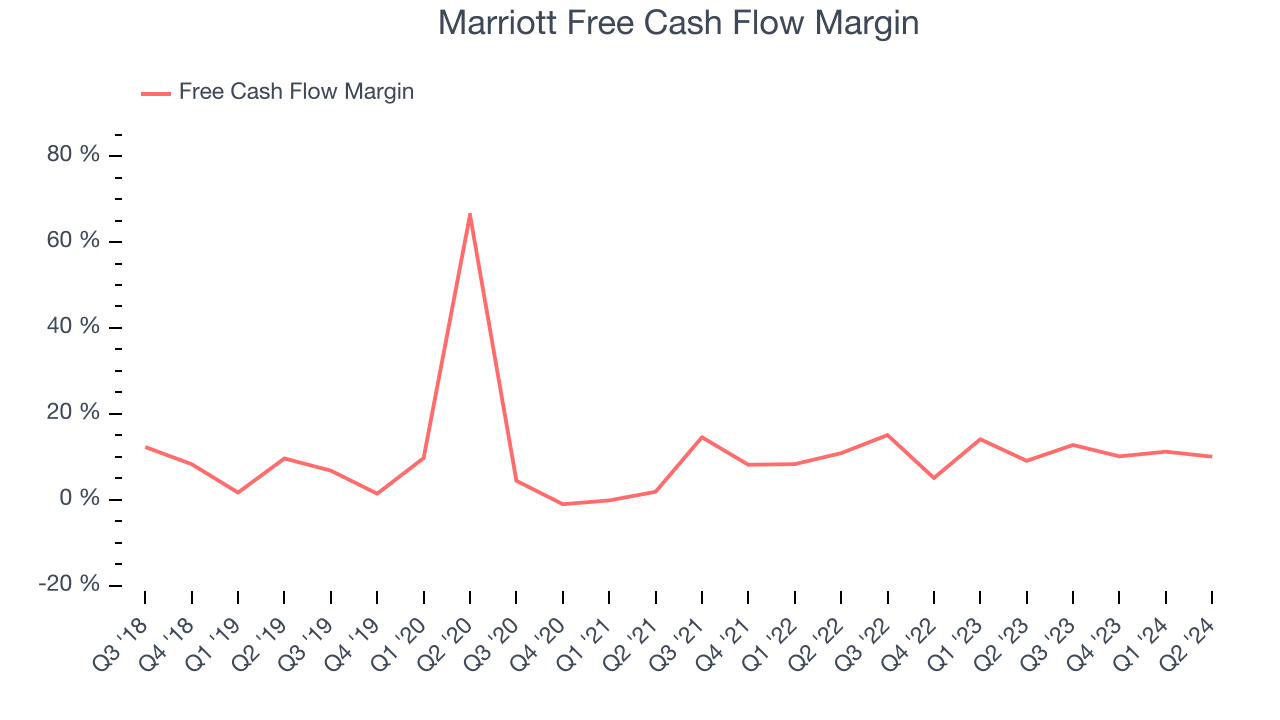

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Marriott has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.3% over the last two years, slightly better than the broader consumer discretionary sector.

Key Takeaways from Marriott’s Q3 Results

We struggled to find many strong positives in these results. Its EPS missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.7% to $251 immediately after reporting.

Marriott may have had a tough quarter, but does that actually create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.