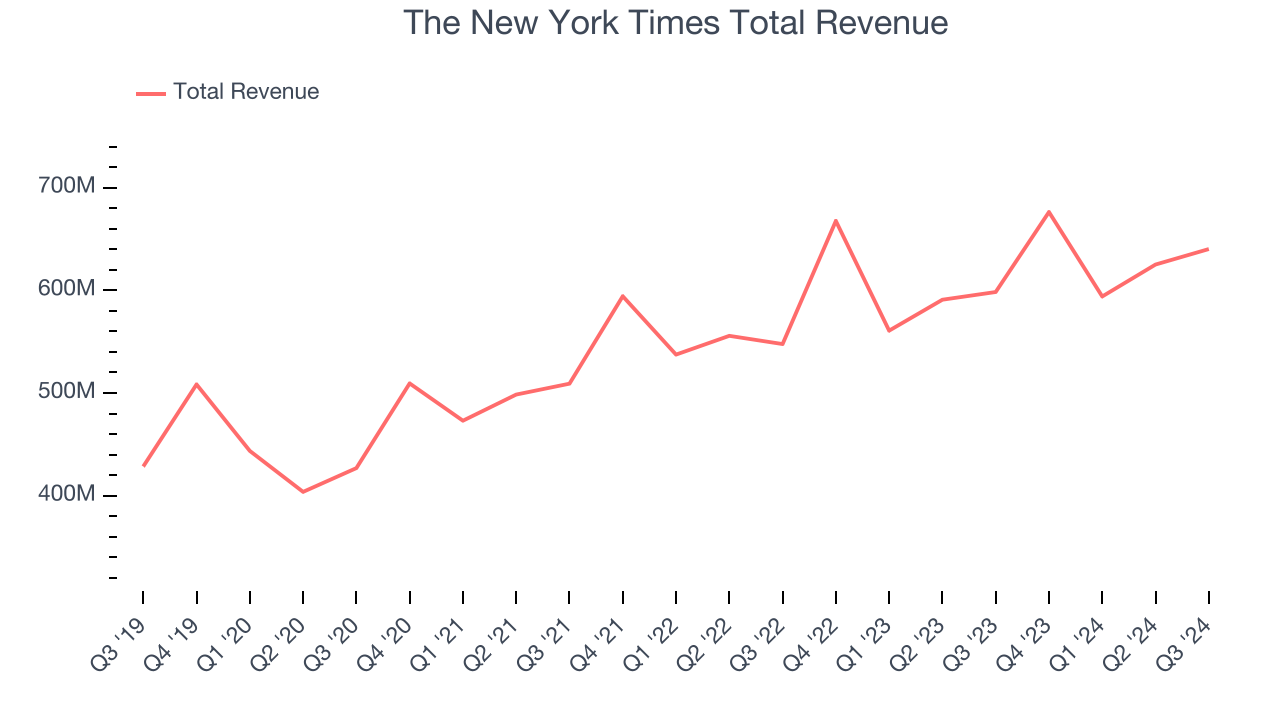

Newspaper and digital media company The New York Times (NYSE:NYT) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 7% year on year to $640.2 million. Its non-GAAP profit of $0.45 per share was 8.9% above analysts’ consensus estimates.

Is now the time to buy The New York Times? Find out by accessing our full research report, it’s free.

The New York Times (NYT) Q3 CY2024 Highlights:

- Revenue: $640.2 million vs analyst estimates of $641 million (in line)

- Adjusted EPS: $0.45 vs analyst estimates of $0.41 (8.9% beat)

- EBITDA: $97.35 million vs analyst estimates of $103.6 million (6.1% miss)

- Gross Margin (GAAP): 48.2%, in line with the same quarter last year

- Operating Margin: 12%, up from 10.6% in the same quarter last year

- EBITDA Margin: 15.2%, in line with the same quarter last year

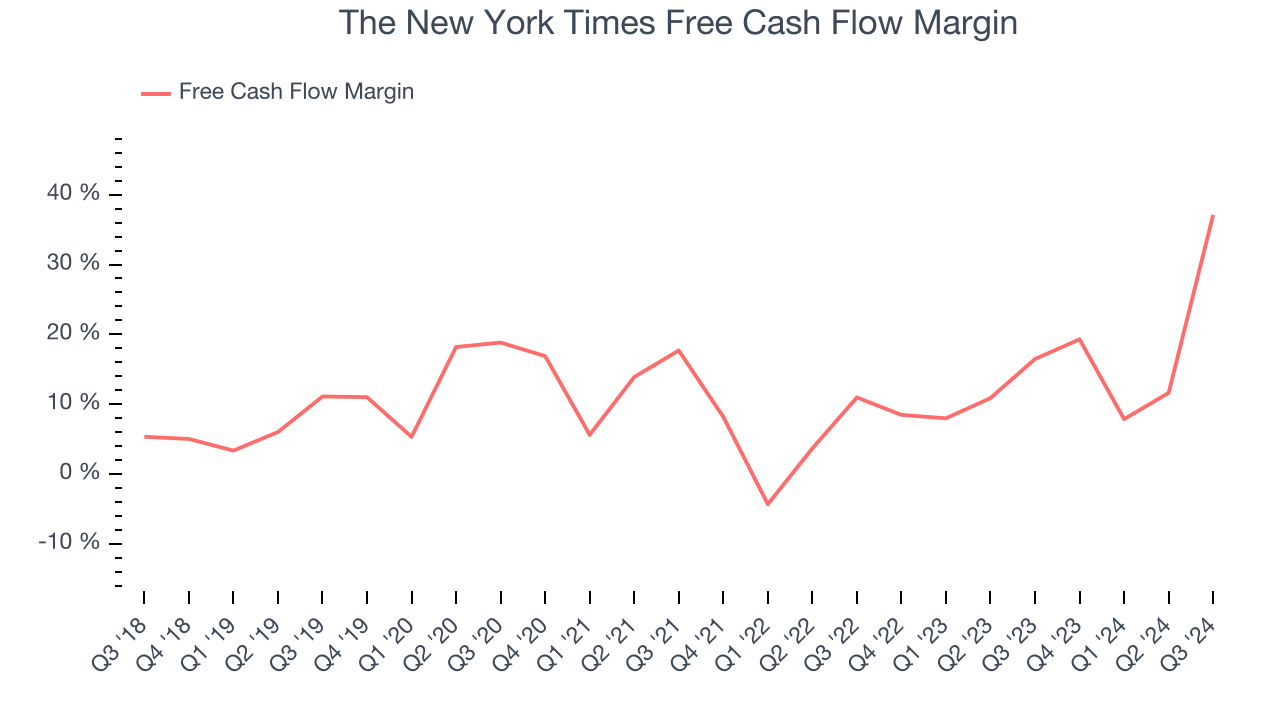

- Free Cash Flow Margin: 37.1%, up from 16.5% in the same quarter last year

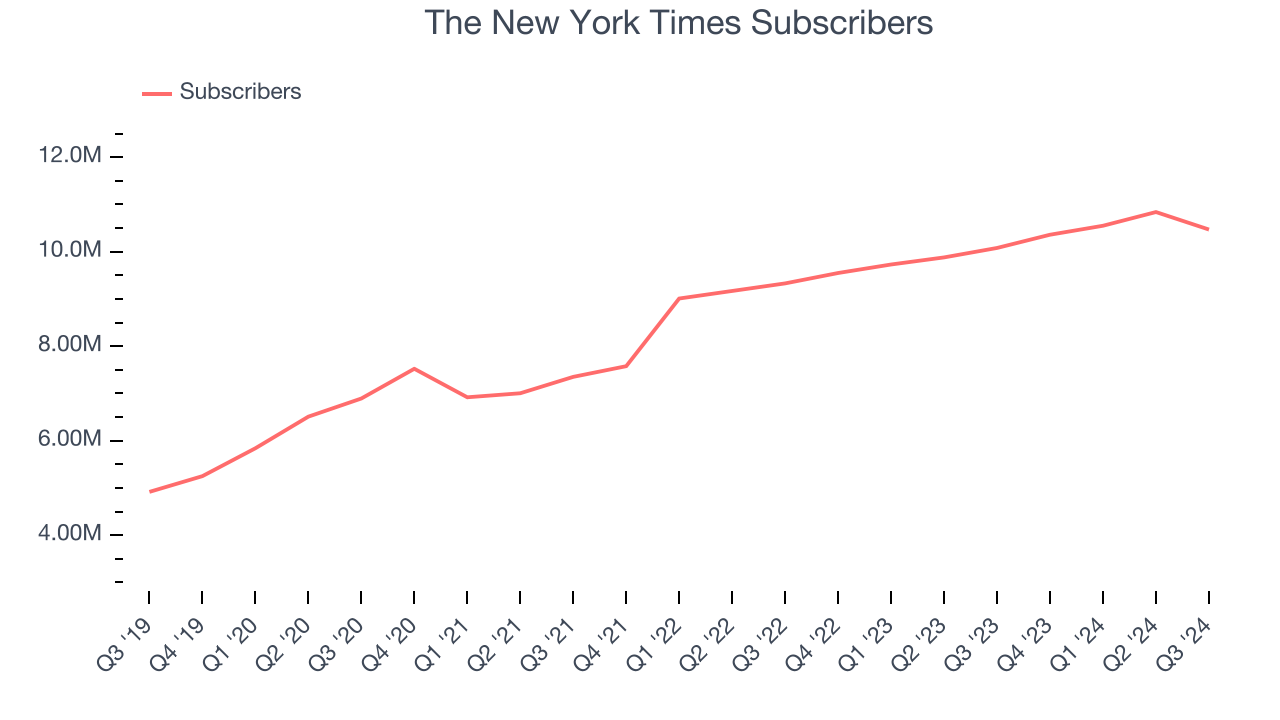

- Subscribers: 10.47 million, up 390,000 year on year

- Market Capitalization: $9.33 billion

Company Overview

Founded in 1851, The New York Times (NYSE:NYT) is an American media organization known for its influential newspaper and expansive digital journalism platforms.

Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Sales Growth

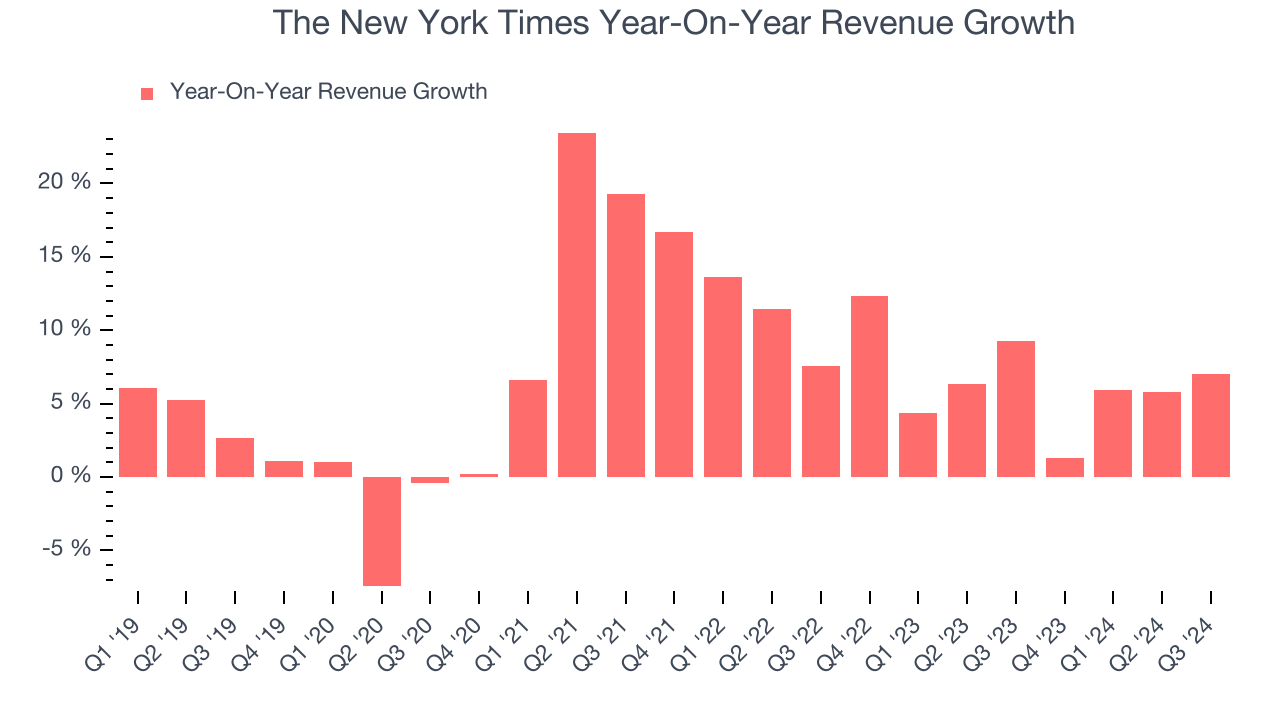

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Unfortunately, The New York Times’s 7% annualized revenue growth over the last five years was sluggish. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. The New York Times’s annualized revenue growth of 6.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s revenue dynamics by analyzing its number of subscribers, which reached 10.47 million in the latest quarter. Over the last two years, The New York Times’s subscribers averaged 10% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, The New York Times grew its revenue by 7% year on year, and its $640.2 million of revenue was in line with Wall Street’s estimates.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

The New York Times has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 15.2% over the last two years, better than the broader consumer discretionary sector.

The New York Times’s free cash flow clocked in at $237.6 million in Q3, equivalent to a 37.1% margin. This result was good as its margin was 20.6 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Key Takeaways from The New York Times’s Q3 Results

It was good to see The New York Times beat analysts’ EPS expectations this quarter. On the other hand, its number of subscribers missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.8% to $55.25 immediately after reporting.

The New York Times underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.