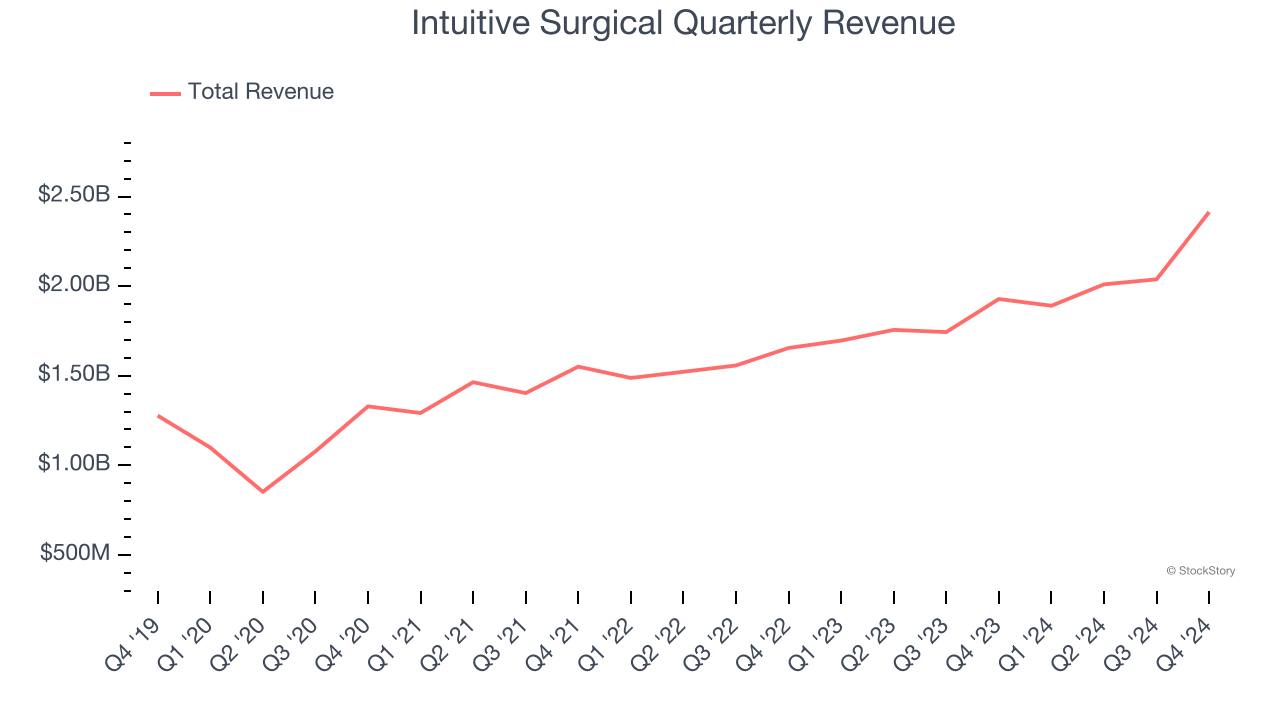

Medical technology company Intuitive Surgical (NASDAQ:ISRG) announced better-than-expected revenue in Q4 CY2024, with sales up 25.2% year on year to $2.41 billion. Its non-GAAP profit of $2.21 per share was 23.8% above analysts’ consensus estimates.

Is now the time to buy Intuitive Surgical? Find out by accessing our full research report, it’s free.

Intuitive Surgical (ISRG) Q4 CY2024 Highlights:

- Revenue: $2.41 billion vs analyst estimates of $2.27 billion (25.2% year-on-year growth, 6.5% beat)

- Adjusted EPS: $2.21 vs analyst estimates of $1.79 (23.8% beat)

- Adjusted EBITDA: $1.06 billion vs analyst estimates of $924.6 million (43.8% margin, 14.2% beat)

- Operating Margin: 30.4%, up from 23.3% in the same quarter last year

- Free Cash Flow was $639.9 million, up from -$207.2 million in the same quarter last year

- Market Capitalization: $206.6 billion

Company Overview

Founded in 1995 as a pioneer in its field, Intuitive Surgical (NASDAQ:ISRG) is a medical technology company best known for its da Vinci robotic surgical systems, which enable minimally invasive surgeries using automation.

Surgical Equipment & Consumables - Specialty

The surgical equipment and consumables industry provides tools, devices, and disposable products essential for surgeries and medical procedures. These companies therefore benefit from relatively consistent demand, driven by the ongoing need for medical interventions, recurring revenue from consumables, and long-term contracts with hospitals and healthcare providers. However, the high costs of R&D and regulatory compliance, coupled with intense competition and pricing pressures from cost-conscious customers, can constrain profitability. Over the next few years, tailwinds include aging populations, which tend to need surgical interventions at higher rates. The increasing integration of AI and robotics into surgical procedures could also create opportunities for differentiation and innovation. However, the industry faces headwinds including potential supply chain vulnerabilities, evolving regulatory requirements, and more widespread efforts to make healthcare less costly.

Sales Growth

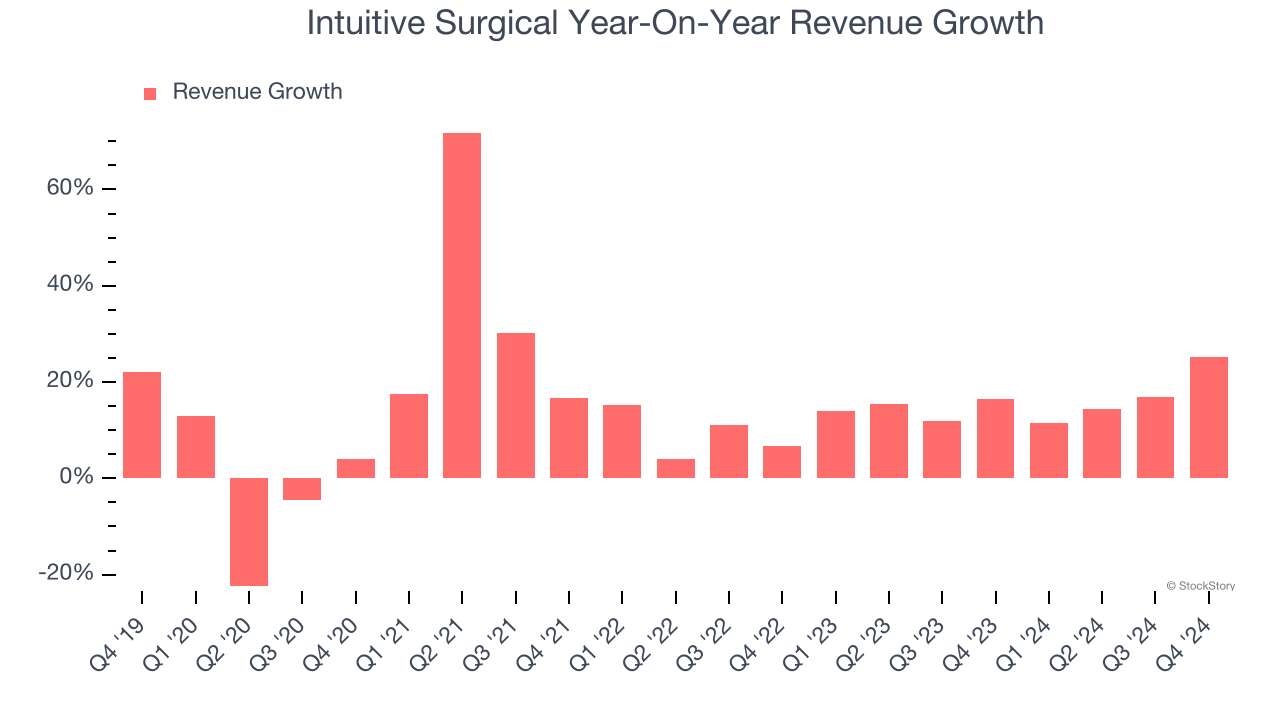

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Intuitive Surgical’s sales grew at a solid 13.3% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Intuitive Surgical’s annualized revenue growth of 15.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Intuitive Surgical reported robust year-on-year revenue growth of 25.2%, and its $2.41 billion of revenue topped Wall Street estimates by 6.5%.

Looking ahead, sell-side analysts expect revenue to grow 14.9% over the next 12 months, similar to its two-year rate. Despite the slowdown, this projection is healthy and implies the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

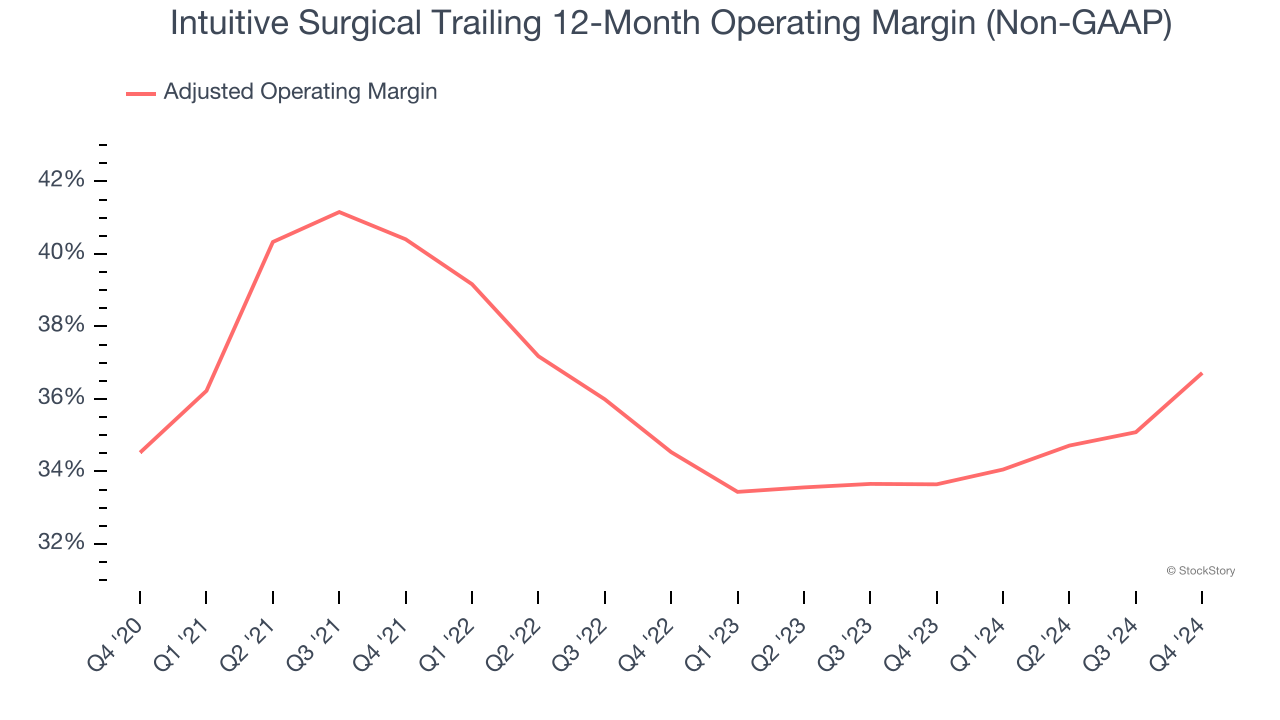

Adjusted Operating Margin

Intuitive Surgical has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 36%.

Looking at the trend in its profitability, Intuitive Surgical’s adjusted operating margin rose by 2.2 percentage points over the last five years, as its sales growth gave it operating leverage. Furthermore, the company’s two-year trajectory shows its performance was mostly driven by its recent improvements. These data points are very encouraging and shows momentum is on its side.

This quarter, Intuitive Surgical generated an adjusted operating profit margin of 38.4%, up 6.2 percentage points year on year. This increase was a welcome development and shows it was recently more efficient because its expenses grew slower than its revenue.

Earnings Per Share

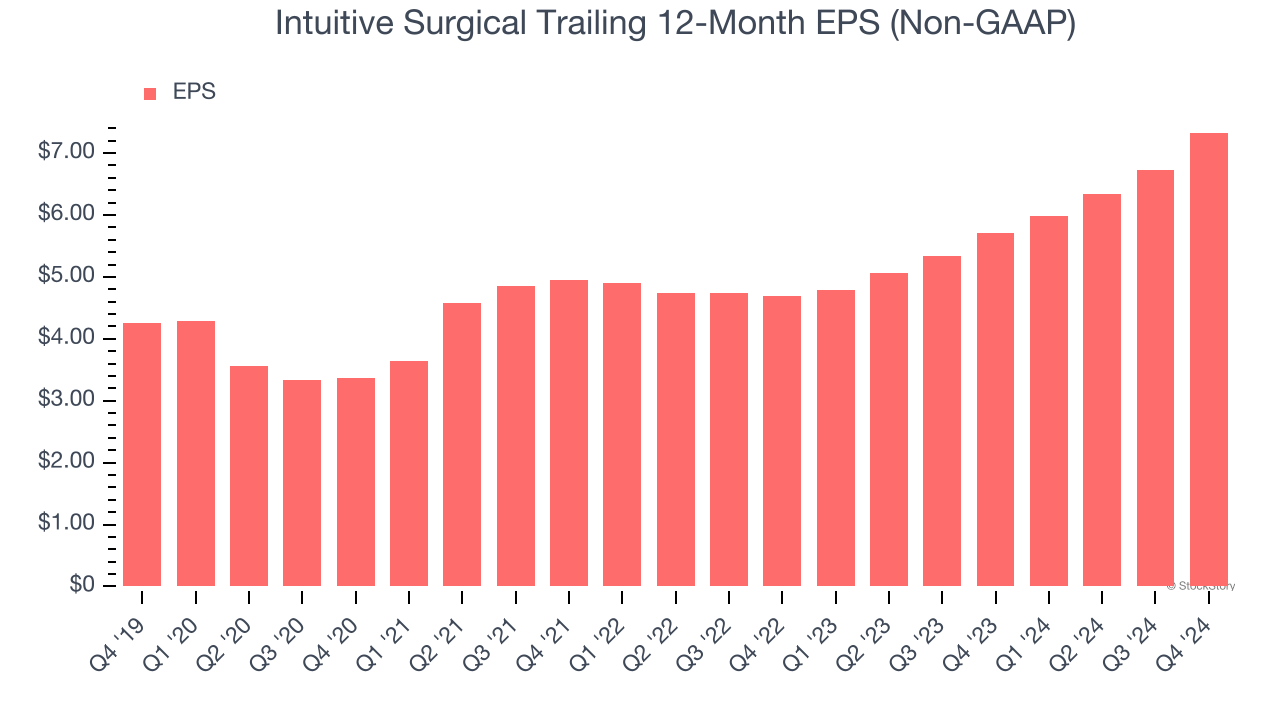

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Intuitive Surgical’s EPS grew at a remarkable 11.5% compounded annual growth rate over the last five years. Despite its adjusted operating margin expansion during that time, this performance was lower than its 13.3% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

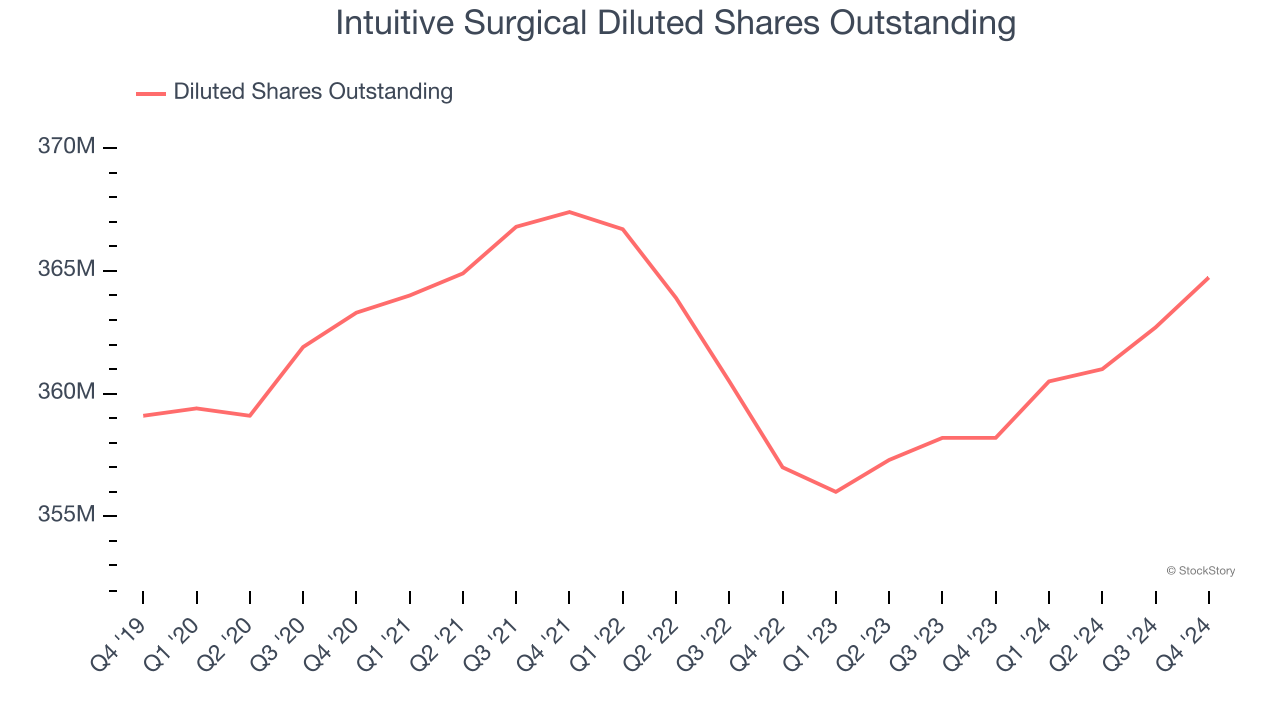

Diving into Intuitive Surgical’s quality of earnings can give us a better understanding of its performance. A five-year view shows Intuitive Surgical has diluted its shareholders, growing its share count by 1.6%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Intuitive Surgical reported EPS at $2.21, up from $1.60 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Intuitive Surgical’s full-year EPS of $7.33 to grow 7.5%.

Key Takeaways from Intuitive Surgical’s Q4 Results

We were impressed by how significantly Intuitive Surgical blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives.

Is Intuitive Surgical an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.