Global pharmaceutical company Pfizer (NYSE:PFE) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 21.9% year on year to $17.76 billion. On the other hand, the company’s full-year revenue guidance of $62.5 billion at the midpoint came in 0.8% below analysts’ estimates. Its non-GAAP profit of $0.63 per share was 37.2% above analysts’ consensus estimates.

Is now the time to buy Pfizer? Find out by accessing our full research report, it’s free.

Pfizer (PFE) Q4 CY2024 Highlights:

- Revenue: $17.76 billion vs analyst estimates of $17.25 billion (21.9% year-on-year growth, 3% beat)

- Adjusted EPS: $0.63 vs analyst estimates of $0.46 (37.2% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $62.5 billion at the midpoint, missing analyst estimates by 0.8% and implying -1.8% growth (vs 10.3% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $2.90 at the midpoint, missing analyst estimates by 1.1%

- Operating Margin: -0.1%, up from -8.7% in the same quarter last year

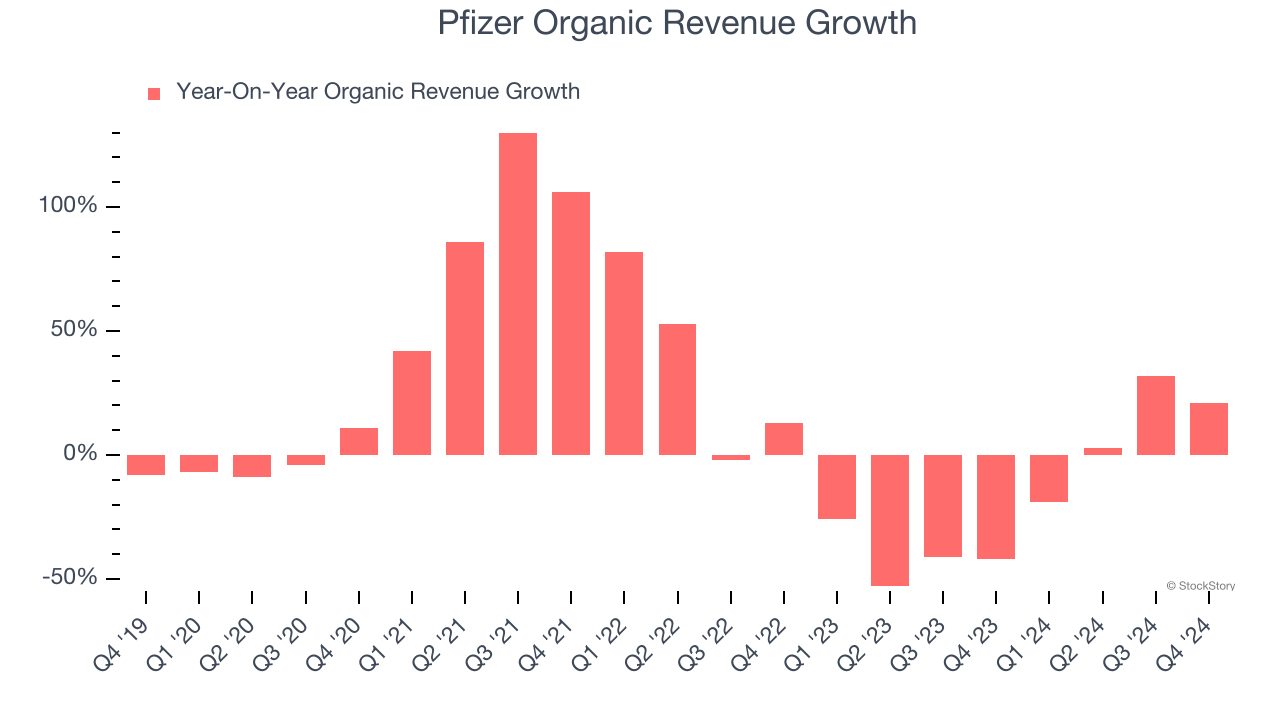

- Organic Revenue rose 21% year on year (-42% in the same quarter last year)

- Market Capitalization: $148.5 billion

Company Overview

Founded in 1849, Pfizer (NYSE:PFE) is a global pharmaceutical company that develops and produces a wide range of medicines and vaccines for various medical conditions.

Branded Pharmaceuticals

The branded pharmaceutical industry relies on a high-cost, high-reward business model, driven by substantial investments in research and development to create innovative, patent-protected drugs. Successful products can generate significant revenue streams over their patent life, and the larger a roster of drugs, the stronger a moat a company enjoys. However, the business model is inherently risky, with high failure rates during clinical trials, lengthy regulatory approval processes, and intense competition from generic and biosimilar manufacturers once patents expire. These challenges, combined with scrutiny over drug pricing, create a complex operating environment. Looking ahead, the industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

Sales Growth

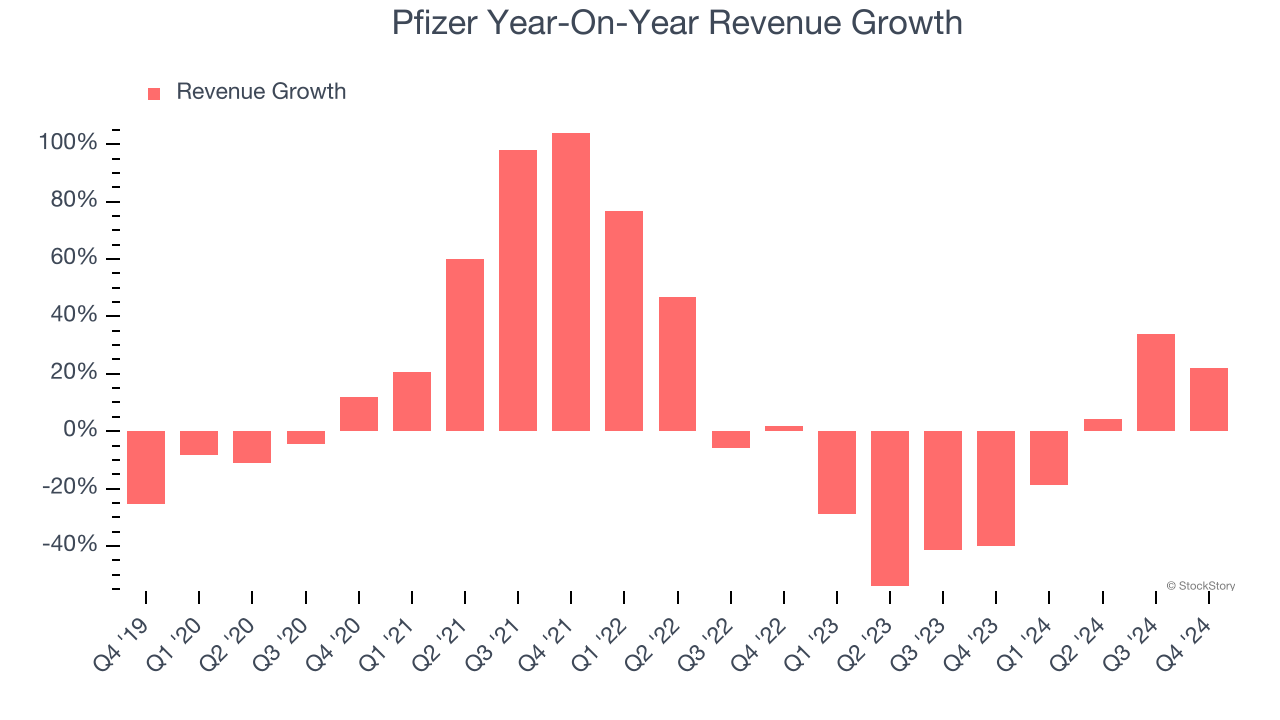

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Pfizer’s sales grew at a mediocre 5.1% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Pfizer’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 20.4% annually.

Pfizer also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Pfizer’s organic revenue averaged 15.6% year-on-year declines. Because this number is better than its normal revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

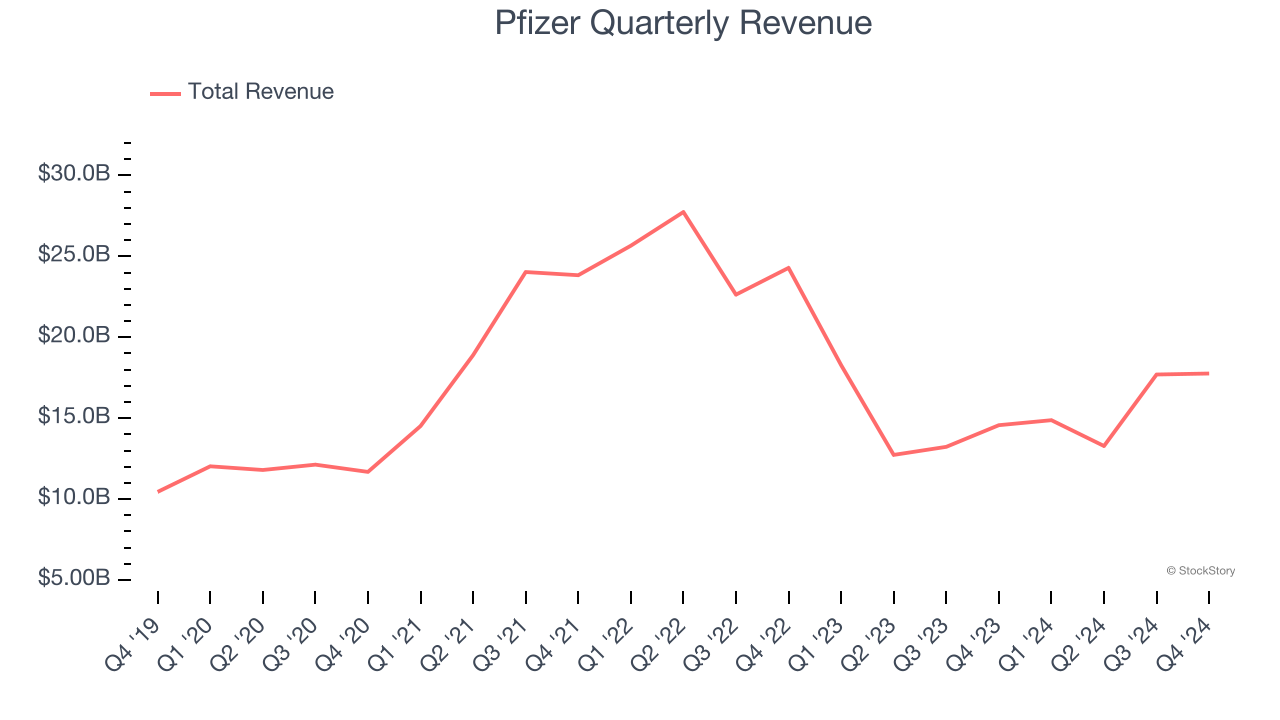

This quarter, Pfizer reported robust year-on-year revenue growth of 21.9%, and its $17.76 billion of revenue topped Wall Street estimates by 3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

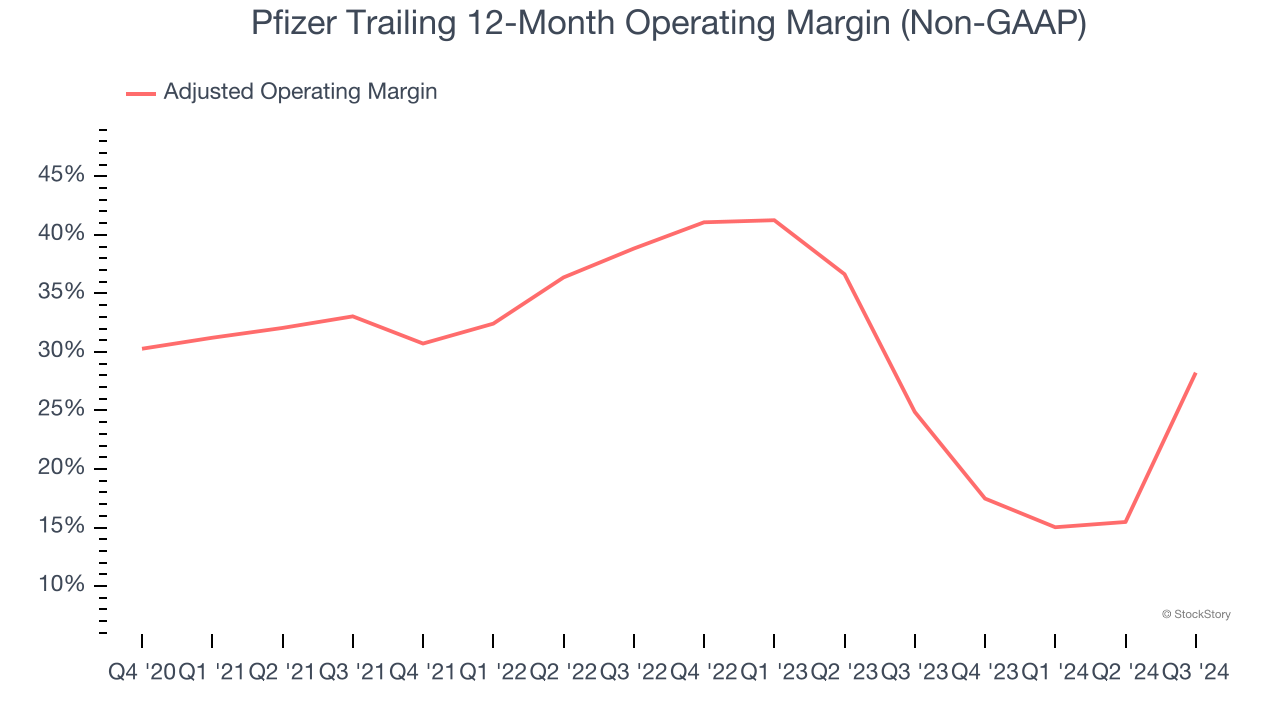

Pfizer has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 32.3%.

Looking at the trend in its profitability, Pfizer’s adjusted operating margin rose by 3.2 percentage points over the last five years. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 8 percentage points on a two-year basis. If Pfizer wants to pass our bar, it must prove it can expand its profitability consistently.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

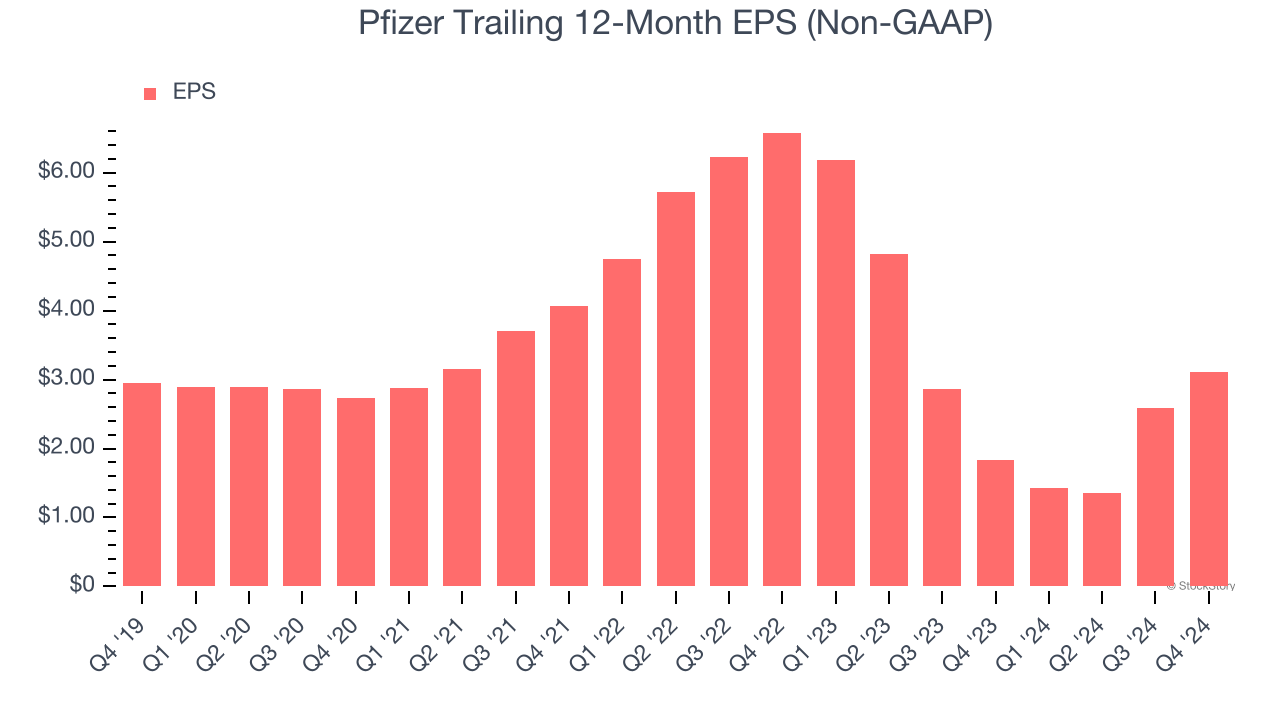

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Pfizer’s EPS grew at an unimpressive 1.1% compounded annual growth rate over the last five years, lower than its 5.1% annualized revenue growth. However, its adjusted operating margin actually expanded during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

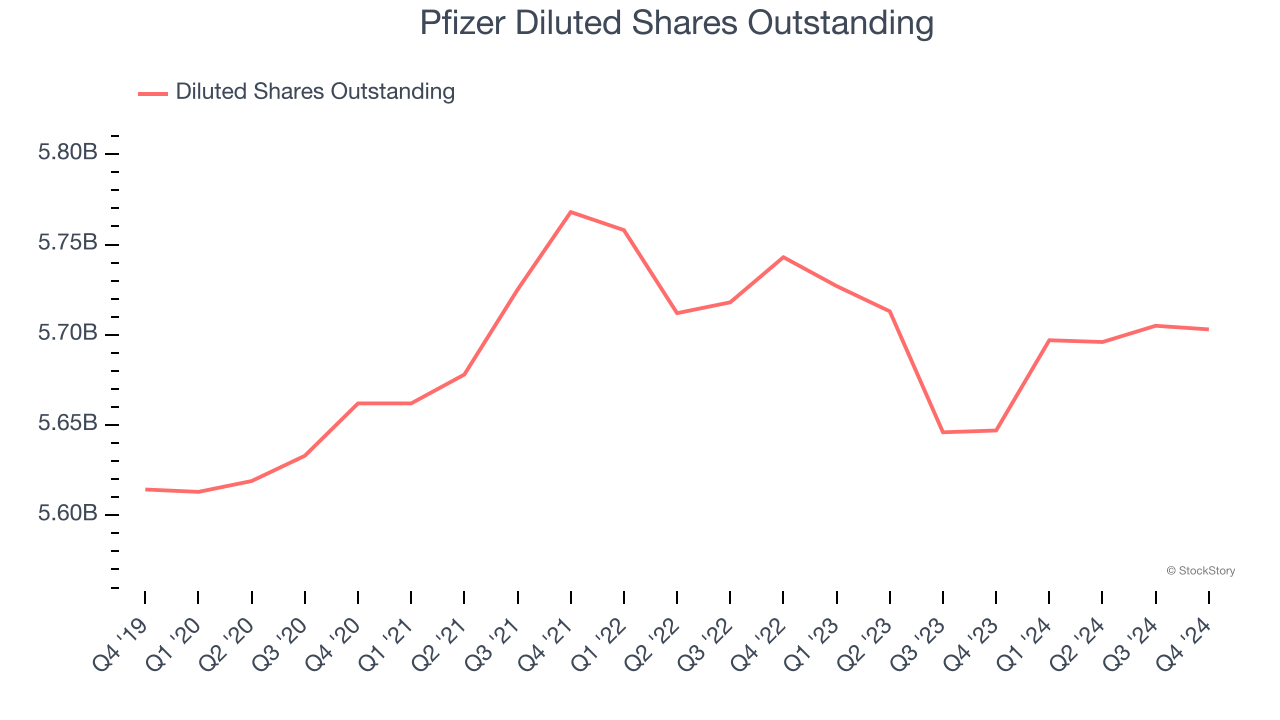

We can take a deeper look into Pfizer’s earnings to better understand the drivers of its performance. A five-year view shows Pfizer has diluted its shareholders, growing its share count by 1.6%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Pfizer reported EPS at $0.63, up from $0.10 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Pfizer’s full-year EPS of $3.11 to shrink by 6.7%.

Key Takeaways from Pfizer’s Q4 Results

We were impressed by how significantly Pfizer blew past analysts’ organic revenue expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EPS guidance slightly missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this quarter was mixed but still had some key positives. The stock traded up 1.7% to $26.68 immediately after reporting.

Sure, Pfizer had a solid quarter, but if we look at the bigger picture, is this stock a buy? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.